Compliance Date Delay

The FDIC is delaying the compliance date for the requirements under 12 CFR 328.4 and 328.5 from May 1, 2025 to March 1, 2026. For more information, please see the Financial Institution Letter (FIL-5-2025).

Below are answers to a collection of questions about the FDIC Official Signs and Advertising Requirements, False Advertising, Misrepresentation of Insured Status, and Misuse of the FDIC’s Name or Logo Final Rule (“final rule”), 12 CFR part 328 (“part 328”). This collection of questions and answers will be periodically updated on the FDIC’s website.

I. Physical Premises

A. FDIC Official Sign

1. With respect to the display of the physical FDIC official sign, does the rule require the FDIC official sign to be posted at a new accounts desk?

Answer: If a banker at a new accounts desk “usually and normally” receives and processes deposits (e.g., processes a check deposit at the new accounts desk), then the official sign must be posted at the new accounts desk. In a scenario where the banker at the new accounts desk always walks the initial deposit over to the teller line, then the teller is “receiving” the deposit and the official sign posted at the teller window is sufficient; therefore, in that situation, an official sign would not be required at the new accounts desk.

(Updated July 15, 2024)

2. Are insured depository institutions (IDIs) required to provide any initial disclosures about FDIC insurance coverage, either orally or in writing, before opening an account?

Answer: No. Part 328 does not require IDIs to provide “initial disclosures” about FDIC coverage before account opening.

(Updated July 15, 2024)

3. Is the FDIC official sign required at night drop facilities?

Answer: No. The official sign is required wherever deposits are usually and normally received. FDIC staff does not view that deposits are usually and normally received by the IDI when placed in a night depository.

(Updated July 15, 2024)

4. The new FDIC official digital sign is generally required to be displayed in the colors navy blue and black. Does the final rule modify the physical FDIC official sign color requirements?

Answer: No. The final rule does not modify color requirements for the physical FDIC official sign. The rule continues to require use of the standard, in-branch official FDIC sign, which is 7x3 inches in size with black lettering and gold background. Upon request, the FDIC will continue to provide the official sign at no cost to IDIs. As has been the case traditionally, IDIs may, at their expense, procure from commercial suppliers signs that vary from the official sign in size, color, or material. An IDI may display signs that vary from the official sign in size, color, or material at any location where display of the official sign is required or permitted. However, any such varied sign that is displayed in locations where display of the official sign is required must not be smaller in size than the official sign, must have the same color for the text and graphics, and include the same content. 12 CFR § 328.3(b)(4).

(Updated July 15, 2024)

5. Is an IDI required to display the FDIC official sign in a drive through location?

Answer: The new rule made no changes to the requirements for drive through lanes. Under part 328, if insured deposits are usually and normally received in areas of the premises other than teller windows or stations, the IDI must display the official sign continuously, clearly, and conspicuously in one or more locations in a manner that ensures a copy of the official sign is large enough so as to be legible from anywhere in those areas. 12 CFR 328.3(b)(2). Because drive through lanes at IDIs can vary greatly, each IDI should assess their situation and apply the requirements under part 328 as appropriate. For example, bank branches may have one or more drive through lane(s) or provide customers with access to ATMs. Part 328.4 provides separate requirements that apply to ATMs that may be located in drive through lanes.

(Updated December 2, 2024)

6. In a small bank branch where there is limited space and where deposit and non-deposit products are offered in the same area, can a banker switch between displaying the FDIC official sign and “non-deposit” signage in the same room when discussing different products?

Answer: Yes. In general, if non-deposit products are offered within an IDI’s premises, the space where those products are offered must be physically segregated from areas where insured deposits are usually and normally accepted. The institution must identify areas where activities related to the sale of non-deposit products occur and clearly delineate and distinguish those areas from the areas where insured deposit-taking activities occur.

In limited situations where physical considerations present challenges to offering non-deposit products in a distinct area from deposit products, IDIs must take prudent and reasonable steps to minimize customer confusion. For example, due to limited space, an IDI that offers both deposit and non-deposit products in the same private office and at the same desk, may switch between displaying the FDIC official sign and non-deposit sign when discussing the relevant product to help minimize customer confusion. However, at no time should a non-deposit sign be displayed in close proximity to the FDIC official sign.

(Updated December 2, 2024)

B. Non-Deposit Signs

1. Is the non-deposit sign required to be displayed in the individual offices within IDIs where non-deposit products are offered?

Answer: Yes. Under 12 CFR § 328.3(c)(2), an IDI must continuously, clearly, and conspicuously display the required non-deposit signage at each location within the premises where non-deposit products are offered. If non-deposit products are offered in individual offices, the non-deposit sign should be visible in those offices.

(July 15, 2024)

II. Digital Channels (e.g., Websites or Apps)

A. Placement and Display of Official Digital Sign

1. Are IDIs' websites considered deposit taking channels for purposes of the digital signage requirements?

Answer: Under part 328, the FDIC official digital sign must be displayed on “digital deposit taking channels,” which includes IDIs’ “websites and web-based or mobile applications that offer the ability to make deposits electronically and provide access to deposits at insured depository institutions.” 12 CFR § 328.5(a). If an IDI’s website is purely informational, with no ability to make deposits or access deposits, it would not be a digital deposit-taking channel.

(Updated July 15, 2024)

2. Can the official digital sign appear only on the IDI’s “home page” and not on the other web pages that make up the website?

Answer: No. Under part 328, the FDIC official digital sign must be displayed on the (1) initial or homepage of the IDI’s website or application, (2) landing or login pages, and (3) pages where a customer may transact with deposits. For example, the FDIC official digital sign should be displayed where a mobile application allows customers to deposit checks remotely, because this electronic space is in effect a digital teller window. 12 CFR § 328.5(d).

(Updated July 15, 2024)

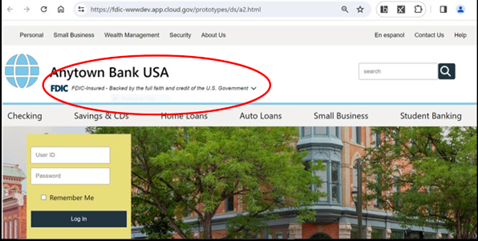

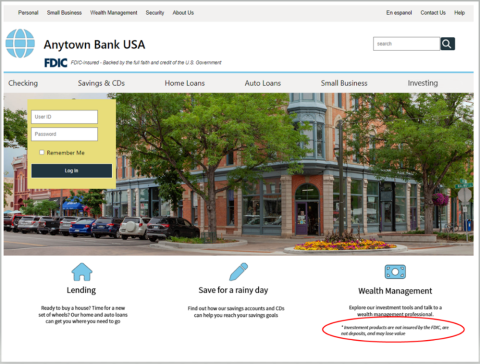

3. Where are we required to place the official digital sign on a bank webpage or app to ensure compliance with the “clear,” “continuous,” and “conspicuous” placement of the digital sign?

Answer: The final rule requires IDIs to display the official digital sign in a clear, continuous, and conspicuous manner. In general, the FDIC would expect to see official digital signs displayed on the applicable pages (see answer II. A. 2.above for the applicable pages) in a manner that is clearly legible to all consumers to ensure they can read it easily. The official digital sign could be displayed above the IDI’s name, to the right of the IDI’s name or below the IDI’s name, but under all circumstances, the official digital sign continuously displayed near the top of the relevant page or screen and in close proximity to the IDI’s name would meet the clear and conspicuous standard under the rule.

Below is an example of the FDIC official digital sign near the top of the page and in close proximity to the IDI’s name:

(Updated July 15, 2024)

4. Can the official digital sign be dismissed once a customer logs in?

Answer: No. The final rule requires that the official digital sign be displayed “in a continuous manner,” which means it must remain visible on the (1) initial page or homepage of the website or application, (2) landing or login pages, and (3) pages where the customer may transact with deposits. 12 CFR § 328.5(d). The final rule, however, does not require the official digital sign to continue to follow the user as they scroll up or down the screen.

(Updated July 15, 2024)

5. Does the official digital sign need to be linked to the FDIC’s website?

Answer: No. Part 328 does not require the official digital sign to be linked to the FDIC’s website. However, it may be helpful to consumers if IDIs link the official digital sign to the FDIC’s optional online BankFind tool, so that consumers can more easily confirm that the bank is FDIC-insured. This would help consumers better differentiate IDIs from non-banks. Optional, downloadable versions of the FDIC official digital sign are accessible to, and available for, bankers on FDICconnect, a secure website operated by the FDIC that FDIC-insured institutions can use to exchange information with the FDIC.

(Updated July 15, 2024)

6. How should IDIs display the FDIC official digital sign on mobile devices with screen resolutions that do not support the ability to display the entirety of the digital sign on one line?

Answer: Generally, the FDIC official digital sign should be displayed as presented (shown below) in the final rule at 12 CFR § 328.5(b), with no alteration to the text except for color variation as noted in the regulation text.

However, if the image does not fit a particular device or screen, the official digital sign can be scaled, “wrapped,” or “stacked” to fit the relevant screen and may satisfy the “clear and conspicuous” requirement.

(Updated July 15, 2024)

7. If an IDI’s name appears at the top of its website, and it also appears in the website’s footer, does the new FDIC official digital sign need to be displayed at the top of the page and also in the footer?

Answer: Under the final rule, IDIs are required to display the FDIC official digital sign “clearly and conspicuously” in a continuous manner; the official digital sign continuously displayed near the top of the relevant page or screen and in close proximity to the IDI’s name would meet the clear and conspicuous standard under the rule. 12 CFR § 328.5(f). IDIs are not required to display the FDIC official digital sign every time the IDI’s name appears, such as in the footer of the website.

(Updated July 15, 2024)

8. To satisfy the final rule’s official digital sign requirements, can the official digital sign be placed in the footer of the webpage?

Answer: No. For purposes of satisfying the final rule, IDIs are required to display the official digital sign in a clear, continuous, and conspicuous manner. The official digital sign continuously displayed near the top of the relevant page or screen and in close proximity to the IDI’s name would meet the clear and conspicuous standard under the rule. 12 CFR § 328.5(f). Therefore, placing the official digital sign in a footer of an IDI’s webpage would not meet the clear, conspicuous, and continuous display requirement.

(Updated July 15, 2024)

9. If an IDI displays the FDIC official digital sign on its mobile app’s homepage and alongside the IDI’s logo within the app, is it also necessary to include this signage on the transaction portal before a customer completes a transaction?

Answer: It depends in part on what type of transaction is being completed. The FDIC official digital sign must be displayed on the (1) initial or homepage of the bank’s website or application, (2) landing or login pages, and (3) pages where a customer may transact with deposits. 12 CFR § 328.5(d). For example, the FDIC official digital sign should be displayed where an IDI’s mobile application allows customers to deposit checks remotely, because this is an electronic space where a customer is transacting with deposits.

However, if a consumer is completing a transaction by using an embedded third-party payment platform that consumers: (a) access after logging into their IDI’s website; and (b) utilize to initiate payments/move funds out of the IDI, then the official digital sign should not be posted on those pages.

(Updated July 15, 2024)

10. What are examples of “pages where the customer may transact with deposits” that require the display of the FDIC official digital sign? Is the digital official sign required on pages where customers transfer funds externally?

Answer: Examples of “pages where the customer may transact with deposits” that require the display of the FDIC official digital sign include: mobile application pages that allow customers to deposit checks remotely; pages where customers may transfer deposits between deposit accounts held within the same IDI (e.g., checking to savings or vice versa); and pages where customers may transfer deposits from an account at the IDI to deposit accounts at other IDIs. On pages where a customer is transferring money from a deposit account to a non-deposit account or where a customer is transferring money from a non-deposit account to a deposit account, the official digital sign is not required. The FDIC is concerned about potential confusion if the official digital sign is displayed where money is being transferred to a non-deposit account. Generally, pages where a logged-in bank customer is initiating external payments (e.g., via bill pay or wire), the official digital sign is not required.

(Updated December 2, 2024)

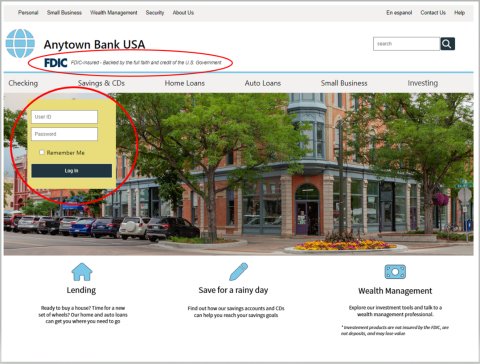

11. What is the definition of “landing or login page”?

For purposes of the final rule, a “landing or login page” generally refers to an insured depository institution’s (IDI’s) webpage or screen from which a customer is able to log into the IDI’s digital deposit taking channel. Specifically, the terms include pages where customers enter their credentials (e.g., username and password) or use other authentication methods (e.g., face identification) to access an IDI’s website or banking application. The terms are intended to cover various types of logins, whether with usernames and passwords, face IDs, thumbprints, etc.

Below is an example of a “landing or login page” of an IDI’s webpage where a customer is able to log in, and where the FDIC official digital sign is near the top of the page and in close proximity to the IDI’s name.

(Updated August 16, 2024)

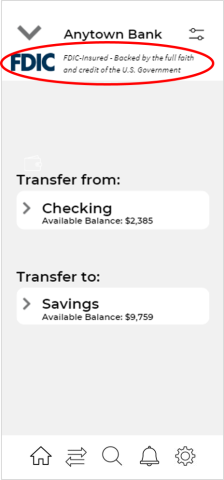

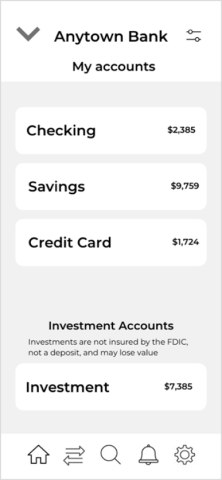

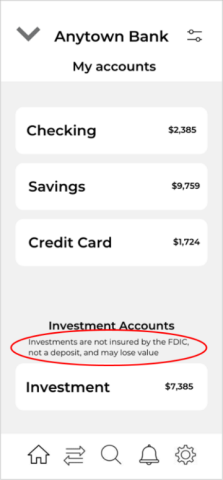

12. Is an IDI required to display the official FDIC digital sign on a dashboard or portal of an IDI’s website or app after the customer logs into the account?

Answer: No. In general, a “dashboard” or “portal” is an account summary webpage or screen on an app that typically displays a customer’s financial information regarding various products after logging in but where a customer does not transact with deposits. For example, a dashboard may provide an overview of an IDI customer’s checking, savings, mortgage, investment, and retirement account balances. For the purposes of part 328, a dashboard or portal as described here is not an initial or homepage, landing or login page, or a page where a customer may transact with deposits. Accordingly, an IDI is not required to display the official FDIC digital sign on such a dashboard or portal. As shown in the example below, the official FDIC digital sign is not displayed in this app version of a dashboard:

(Updated August 16, 2024)

13. Where should the official digital sign be placed if the IDI’s app or website does not currently display the IDI’s full name; it only displays the IDI’s logo or a partial name?

Answer: The final rule provides that an official digital sign be continuously displayed near the top of the relevant page or screen and in close proximity to the IDI’s name would be considered clear and conspicuous. 12 CFR § 328.5(f)

If an IDI displays its full name, a partial name of the IDI, or the logo of the IDI (or any similar symbol used to identify the IDI) near the top of the page or screen, and continuously displays the official digital sign in close proximity to it, this approach would be considered clear and conspicuous.

(Updated August 16, 2024)

14. How should IDIs incorporate the digital sign on mobile devices in accordance with part 328’s requirements while also remaining ADA compliant?

Answer: The final rule does not supersede or alter the requirements of IDIs to comply with ADA’s digital accessibility rules. As IDIs implement the final rule’s requirements, IDIs should take steps ensure that their web content is fully compliant with other laws and regulations.

(Updated August 16, 2024)

15. Do the FDIC official digital sign requirements apply to downloadable content such as terms and conditions or other digital collateral available via an IDI’s online channels?

Answer: Part 328 requires IDIs to display the official digital sign on their digital deposit-taking channels on the following pages or screens: initial or homepage of the website or application, landing or login pages, and pages where the customer may transact with deposits. Downloadable content that is available from an IDI’s website would not likely be viewed as a page or screen where the official digital sign would be required.

(Updated August 16, 2024)

16. Is an IDI required to display the FDIC official digital sign in the app store where the IDI’s app is available for download?

Answer: No. An IDI is not required to post the official digital sign in the app store where its app is available for download.

(Updated August 16, 2024)

17. How are affiliated entities treated for the purpose of complying with the requirement under 12 CFR 328.5(g)(2) for a “one-time notification” for bank customers related to a third party’s non-deposit products?

Answer: If an IDI’s digital deposit taking channel offers a third party’s non-deposit product (e.g., investments or insurance) that requires the logged-in bank customer to leave the IDI’s deposit taking channel (e.g., a website) and access the non-deposit product on the third party’s online platform, then the IDI will be required to provide the bank customer with a “one time” notification per web session before the customer leaves the IDI’s digital deposit-taking channel. See 12 CFR 328.5(g)(2). The notification must be dismissed by an action of the bank customer before initially accessing the third party’s online platform and it must clearly and conspicuously indicate that the third party’s non-deposit products: are not insured by the FDIC; are not deposits; and may lose value. The IDI may include additional disclosures in the notification that may help prevent consumer confusion, including, for example, that the bank customer is leaving the IDI’s website

For the purposes of 12 CFR 328.5(g)(2), the FDIC views affiliated entities as “third parties” consistent with the 2023 Interagency Guidance on Third-Party Relationships: Risk Management.

(Updated December 2, 2024)

18. Is it permissible to translate the FDIC official digital sign into Spanish or another language other than English, and still be in compliance with part 328?

Answer: Under part 328, the FDIC official digital sign consists of ‘‘FDIC’’ along with the following text: ‘‘FDIC-Insured- Backed by the full faith and credit of the U.S. Government.’’ The design and display of the digital sign is specified under § 328.5 as the following:

IDIs must include the official digital sign as provided in the part 328. IDIs, however, may, in addition to the required official digital sign, provide a translation of the official digital sign in another language. An IDI displaying solely a translated digital sign would not meet the requirements of part 328.

(Updated December 2, 2024)

19. Does the final rule require that an IDI link the FDIC official digital sign to the FDIC’s Electronic Deposit Insurance Estimator (EDIE)?

Answer: No, the final rule does not require IDIs to link the official digital sign to the FDIC’s EDIE. The FDIC's EDIE is an online tool that can be used to determine whether a deposit account is fully insured at each IDI where the consumer’s deposits are held. Part 328 does not require the FDIC official digital sign to be linked to the EDIE website. However, it may be helpful to consumers if IDIs choose to link the official digital sign to EDIE, so that consumers can more easily access additional information about deposit insurance, such as calculating insurance coverage of deposit accounts at IDIs and confirming information about how the deposit insurance rules and limits apply.

The optional, downloadable versions of the FDIC official digital sign are accessible to, and available for, bankers on FDICconnect, a secure website operated by the FDIC that FDIC-insured institutions can use to exchange information with the FDIC. The optional versions also include links to BankFind and EDIE.

(Updated December 2, 2024)

20. When a bank offers commercial customers batch check depositing services through Remote Deposit Capture where a commercial customer logs into a non-bank website or app and accesses a non-bank online portal to deposit checks, is the official digital sign required?

Answer: No. A nonbank company is prohibited from using FDIC-Associated Terms or FDIC-Associated Images, this includes using the official FDIC digital sign, in a manner that inaccurately states or implies that a person other than an IDI is insured by the FDIC. 12 CFR § 328.102 (b)(1)(iv). Only IDIs may display the FDIC official digital sign on their digital deposit-taking channels under 12 CFR § 328.5 (d).

(Updated December 2, 2024)

21. Is the official digital sign required on a bank webpage or other digital channel that accepts account opening applications?

Answer: No, the official digital sign is not required on a bank webpage or other digital channel that accepts account opening applications

(Updated December 2, 2024)

22. Are sweep accounts considered non-deposit products or uninsured deposit products for purposes of part 328’s digital sign requirement? In other words, should the digital sign be displayed on digital channels where customers can transact in sweep accounts?

Answer: Sweep accounts can vary. For example, banks typically offer business overnight sweep accounts where money is swept from traditional business deposit checking accounts into overnight investment accounts that are not FDIC-insured but are bank-collateralized. Such sweep accounts are considered “hybrid products” under the final rule. 12 CFR 328.1. The final rule does not require that IDIs display either the FDIC digital sign or non-deposit signage on pages relating to “hybrid products.” However, IDIs should be following the customer disclosure requirements related to the insurability of sweep accounts under 12 CFR 360.8(e).

(Updated December 2, 2024)

B. Non-Deposit Signs

1. On IDIs’ webpages or apps where IDIs are required to display the non-deposit sign, where should the non-deposit sign be displayed?

Answer: An IDI must clearly and conspicuously display a non-deposit sign on each page relating to non-deposit products if the IDI offers both access to deposits and non-deposit products. This signage must be displayed continuously on each page relating to non-deposit products.

Regarding placement of the sign, an example of clear and conspicuous placement of the non-deposit sign is to place it in close proximity to where access to a non-deposit product is provided on each page relating to non-deposit products.

(Updated August 16, 2024)

2. Would you explain the requirement for a “one-time notification” before a customer accesses a third-party website?

Answer: If an IDI’s digital deposit-taking channel, such as a website, offers access to non-deposit products from a non-bank third party’s online platform, and a logged-in IDI customer attempts to access such non-deposit products, an IDI must provide a one-time per web-session notification on the IDI’s deposit-taking channel before the customer leaves the IDI’s digital deposit-taking channel. The one-time notification could include, for example, an IDI using a “pop-up”, “speedbump”, or “overlay” that must be dismissed by an action of the IDI’s customer before initially accessing the third party’s online platform.

The notification must clearly and conspicuously indicate that the third party’s non-deposit products: are not insured by the FDIC; are not deposits; and may lose value. 12 CFR § 328.5(g)(2). The IDI may include additional disclosures in the notification that may help prevent consumer confusion, including, for example, that the IDI customer is leaving the IDI’s website.

(Updated August 16, 2024)

3. Does the requirement for a non-deposit “one-time notification” before a customer accesses a third-party website need to appear twice in the same session, if the customer clicks on the same link twice?

Answer: No. If an IDI customer who is logged into an IDI’s digital deposit-taking channel (such as an IDI’s website and app) clicks on a hyperlink that takes them to a third-party's website and then the customer clicks on the same hyperlink again in the same session, the IDI would only be required to provide the one-time notification the first time the customer clicks the link, and not each subsequent time that the customer clicks on the same link in the same session.

On the other hand, the notification should be given twice during the same session if a consumer clicks on a link to access a third-party website and then in the same session clicks on a different link that takes them to a different third party’s website.

(Updated August 16, 2024)

4. Would displaying a shortened version of the Interagency Statement on Retail Non-Deposit Investments disclosure as a footer on a webpage satisfy the requirements of the FDIC non-deposit sign?

Answer: A shortened version of the Retail Non-Deposit Investments disclosure (“not FDIC insured; no bank guarantee; may lose value”) can be substituted for the non-deposit sign (“are not insured by the FDIC; are not deposits; and may lose value”), as long as the language is displayed clearly, conspicuously, and continuously on each webpage relating to non-deposit products and other applicable requirements of the rule are adhered to.

For example, this signage may not be displayed in close proximity to the official FDIC digital sign. In addition, placing the sign in a footer of an IDI’s webpage would not meet the clear, conspicuous, and continuous display requirement.

(Updated August 16, 2024)

5. If an IDI identifies instances on its website where a consumer could be confused about a product offering or other issues, does the IDI have flexibility to provide additional clarifying information to consumers?

Answer: Yes. If an IDI has satisfied the final rule’s requirements, it may provide additional or supplemental clarifying disclosures to consumers on its digital channels.

(Updated August 16, 2024)

6. On which webpages should IDIs include non-deposit signs and are we in compliance if we place the non-deposit signs in the footer of the webpage?

Answer: With respect to which specific webpages the non-deposit signs must be displayed, when an IDI offers both access to deposits and non-deposit products on its digital deposit-taking channels, it must display a non-deposit sign indicating that non-deposit products: are not insured by the FDIC; are not deposits; and may lose value. This non-deposit sign must be displayed clearly, conspicuously, and continuously on each page relating to non-deposit products.

With respect to whether the non-deposit signs can be placed in the footer, although there is no requirement for the non-deposit sign to be displayed near the top of the relevant page or screen, placing the non-deposit sign in a footer of an IDI’s webpage would generally not meet the clear, conspicuous, and continuous display requirement. In addition, the non-deposit products sign may not be displayed in close proximity to the FDIC official digital sign. 12 CFR § 328.5(g)(1).

(Updated July 15, 2024)

7. When disability insurance or credit insurance is added to a loan, such as a car loan, does the bank need to post the ‘not FDIC insured’ sign?

Answer: Generally, FDIC staff has viewed credit life insurance as well as disability insurance as part of the offering of credit. Under 12 CFR 328.1, the definition of “non-deposit product” does not include “credit products” which means the non-deposit sign is not required when an IDI offers credit products.

(Updated December 2, 2024)

8. Is an IDI required to display the non-deposit sign on a bank’s navigation menu near a link to a non-deposit product page, and provide a one-time notification, such as a pop-up screen?

Answer: No, an IDI is not required to display the non-deposit sign on a bank’s navigation menu near a link to a non-deposit product page. A navigation menu or webpage banner is typically displayed as a horizontal bar near the top of a bank’s initial or homepage. A bank’s name and logo are often displayed near a navigation menu. The navigation menu or website banner generally lists several products or services (e.g., Checking, Savings and CDs, Home Loans, Auto Loans, Small Business, Investing). Given that pursuant to part 328’s requirements, a bank’s navigation menu would likely be located in close proximity to the official FDIC digital sign, an IDI would not be expected to display the non-deposit sign near a non-deposit product displayed on the navigation menu.

For logged-in bank customers, an IDI would be required to provide a one-time notification, such as a “pop-up,” speedbump," or "overlay", if the link offers access to non-deposit products from a non-bank third party’s online platform. 12 CFR 328.5(g)(2). The IDI may include additional disclosures in the notification that may help prevent consumer confusion, including, for example, that the IDI customer is leaving the IDI’s website (see answer II.B.2 for the "one-time notification" requirement).

(Updated December 2, 2024)

C. Use of Advertising Statement on Digital Channels

1. Should IDIs include the “Member FDIC,” “Member of FDIC,” or “FDIC-Insured” advertising statement on every page of their digital platforms?

Answer: The advertising statement (e.g., “Member FDIC”) must be displayed on advertisements, consistent with 12 CFR § 328.6. It is not intended to overlap with the official digital sign, and the advertising statement is not required on web pages where an IDI displays the official digital sign, such as the bank’s homepage. However, an IDI is not prohibited from displaying the advertising statement on a page that also includes the official digital sign, so long as the use of the advertising statement on that page is otherwise consistent with the official advertising statement requirements in 12 CFR § 328.6.

(Updated July 15, 2024)

2. If a customer clicks on a hyperlink on an IDI’s webpage to get marketing information about specific deposit products, would such a marketing page that a customer subsequently views require the FDIC official digital sign?

Answer: Advertising pages (i.e., commercial messages, in any medium, that is designed to attract public attention or patronage to a product or business) must adhere to the requirements of 12 CFR § 328.6, which requires the inclusion of an official advertising statement, either “Member of the Federal Deposit Insurance Corporation”, or a short title of “Member of FDIC”, “Member FDIC”, “FDIC-insured”, or a reproduction of the FDIC’s symbol. IDIs are not required to display the official FDIC digital sign on advertising pages.

(Updated August 16, 2024)

3. Can the FDIC provide a translation of the new “FDIC-Insured” optional short title of the official advertising statement?

Answer: Under the final rule, IDIs have the option to use ‘‘FDIC-Insured’’ as a short form of the official advertising statement to satisfy advertising statement requirements under 12 CFR 328.6. Under part 328, a non-English equivalent of the official advertising statement may be used in any advertisement, provided that the translation has the prior written approval of the FDIC. In the preamble to the final rule, the FDIC indicated that it was considering making available to the public approved translations of the official advertising statement in several common languages in the future to support IDIs’ efforts to communicate with their non-English-speaking customers.

Below please find the translation of the new optional short title, “FDIC-Insured,” in 26 non-English languages that IDIs may use as the official advertising statement pursuant to part 328. For convenience, the FDIC is also providing the 26 non-English translations of the other optional short titles “Member FDIC” and “Member of FDIC.”

(Updated December 2, 2024)

Translation of “FDIC-Insured”

| Language | Translation |

|---|---|

| Arabic | FDIC مؤمَّن عليه من قبل |

| Bengali | FDIC বীমাকৃত |

| Burmese | FDIC တွင်အာမခံထားရှိသည် |

| Chinese (Traditional – ZHHK) | FDIC 承保 |

| Chinese (Simplified – ZHTW) | FDIC 承保 |

| Dari | بیمه شده FDIC |

| Haitian Creole | FDIC Asire |

| French (France) | Assuré par la FDIC |

| German | FDIC-versichert |

| Greek | Με ασφάλιση FDIC |

| Gujarati | FDIC દ્વારાવીમાથી આરક્ષિત |

| Hindi | FDIC बीमित |

| Italian | Assicurato FDIC |

| Hmong | Muaj Kev Pov Hwm Los Ntawm FDIC |

| Japanese | FDIC 預金保護対象 |

| Korean | FDIC 보험에 가입됨 |

| Pashto | د FDIC لخوا بيمه شوی |

| Polish | Ubezpieczony przez FDIC |

| Portuguese (Brazil) | Segurado pela FDIC |

| Russian | Застрахован FDIC |

| Ukrainian | Застрахований FDIC |

| Spanish | Asegurado por la FDIC |

| Swahili | Imelipiwa bima na FIDC |

| Tagalog (Philippines) | Nakaseguro sa FDIC |

| Vietnamese | Được FDIC Bảo Hiểm |

| Urdu | FDICسےانشورنس یافتہ |

Translation of “Member FDIC”

| Language | Translation |

|---|---|

| Arabic | FDIC عضو |

| Bengali | FDIC সদস্য |

| Burmese | FDIC မန်ဘာအဖွဲ့ဝင် |

| Chinese (Traditional – ZHHK) | FDIC 成員銀行 |

| Chinese (Simplified – ZHTW) | FDIC 成员银行 |

| Dari | عضو FDIC |

| Haitian Creole | Manm FDIC |

| French (France) | Membre de la FDIC |

| German | Mitglied FDIC |

| Greek | Μέλος FDIC |

| Gujarati | FDIC સભ્ય |

| Hindi | सदस्य FDIC |

| Italian | Membro FDIC |

| Hmong | Tswv Cuab rau FDIC |

| Japanese | FDIC 加盟銀行 |

| Korean | FDIC 회원 |

| Pashto | FDIC غړی |

| Polish | Członek FDIC |

| Portuguese (Brazil) | Membro da FDIC |

| Russian | Член FDIC |

| Ukrainian | Член FDIC |

| Spanish | Miembro FDIC |

| Swahili | Mwanachama wa FDIC |

| Tagalog (Philippines) | Miyembro ng FDIC |

| Vietnamese | Thành Viên FDIC |

| Urdu | FDIC ممبر |

Translation of “Member of FDIC”

| Language | Translation |

|---|---|

| Arabic | ﻋﺿو FDIC |

| Bengali | FDIC এর সদস্য |

| Burmese | FDIC ၏မန်ဘာအဖဲွ�ဝင် |

| Chinese (Traditional – ZHHK) | FDIC 成員銀行 |

| Chinese (Simplified – ZHCN) | FDIC 成员银行 |

| Dari | ﻋﺿو FDIC |

| Haitian Creole | Manm FDIC |

| French (France) | Membre de la FDIC |

| German | Mitglied der FDIC |

| Greek | Μέλος της του FDIC |

| Gujarati | FDIC ના સભ્ય |

| Hindi | FDIC का सदस्य |

| Italian | Membro della FDIC |

| Hmong | Tswv Cuab ntawm FDIC |

| Japanese | FDIC 加盟銀行 |

| Korean | FDIC 회원 |

| Pashto | د FDIC ﻏړی |

| Polish | Członek FDIC |

| Portuguese (Brazil) | Membro da FDIC |

| Russian | Член FDIC |

| Ukrainian | Член FDIC |

| Spanish | Miembro de la FDIC |

| Swahili | Mwanachama wa FDIC |

| Tagalog (Philippines) | Miyembro ng FDIC |

| Vietnamese | Thành Viên của FDIC |

| Urdu | FDICکا ممبر |

D. Automated Teller Machines or Like Devices

1. When implementing new official digital signage on ATMs, are IDIs required to remove existing physical signs, or can both types of signage be displayed simultaneously?

Answer: IDIs are not required to take down physical FDIC official signs attached to ATMs. For an IDI’s ATM or like device that receives deposits but does not offer access to non-deposit products, except as described below, the final rule provides flexibility to meet the signage requirement by either (1) displaying the FDIC official digital sign electronically on ATM screens (consistent with the image as described in 12 CFR § 328.5), or (2) displaying the physical official sign by attaching or posting it to the ATM.

However, IDIs’ ATMs or like devices that accept deposits and are put into service after January 1, 2025, must display the official digital sign electronically (with no option to satisfy the requirement through display of the physical official sign). 12 CFR § 328.4(e).

(Updated July 15, 2024)

2. If an IDI’s ATM accepts deposits but does not accept non-deposit products, on what pages or screens are IDIs required to post or display official FDIC signs?

Answer: For ATMs currently in service, or that will be put into service on or before January 1, 2025, under 12 CFR § 328.4 (b), “an insured depository institution’s automated teller machine or like device that receives deposits” but “does not offer access to non-deposit products” may comply with the official sign requirement in one of two ways.

The first option is to post or attach the physical official FDIC sign (as described in 12 CFR § 328.2) on the ATMs. For IDIs that select this option, it is worth noting that a “degraded or defaced physical official sign” would not satisfy the “clearly, continuously, and conspicuously” requirement for purposes of 12 CFR § 328.4(b)(1). See 12 CFR § 328.4(f).

The second option is to display the FDIC official digital sign as described in § 328.5 on its ATMs home pages or screens and on each transaction page or screen relating to deposits.

The regulation does not provide an exhaustive list of what constitutes “each transaction page or screen relating to deposits.” However, to provide an example, if an IDI’s customer is depositing funds at the IDI’s ATMs, then the final rule requires display of the FDIC official digital sign on pages related to that transaction. Similarly, if an IDI’s customer is transferring funds between deposit accounts at their IDI’s ATM, then the digital official sign is required on those transaction pages or screens.

In contrast, if an IDI customer is only checking their balance, those pages/screens are not “transaction” pages for purposes of Part 328; therefore, a digital official sign is not required on those non-transaction pages.

(Updated August 16, 2024)

3. For an IDI’s deposit taking ATM, is the IDI required to post the FDIC official digital sign or the non-deposit sign when an ATM or debit card from another institution is used to log into an ATM?

Answer: In general, an IDI’s ATM or like device that receives deposits and offers access to non-deposit products must clearly, continuously, and conspicuously display the official FDIC digital sign (as described in 328.5) on its home page or screen and on each transaction page or screen relating to deposits. An insured depository institution’s ATM or like device that receives deposits and does not offer access to non-deposit products may comply with the official sign requirement by either: (1) displaying the physical official sign on the ATM; or (2) displaying the FDIC official digital sign.

However, in some cases an IDI’s ATM may allow a non-customer to use a debit card or credit card from another financial institution (including other IDIs, credit unions, or other financial entities), which allows the non-customer to check their balance, withdraw funds or add funds to their accounts. For such circumstances, the IDI’s ATM may be unable to identify or verify non-customer information, including whether the non-customer is accessing FDIC-insured deposit accounts, or non-deposit products. In this scenario, if the IDI is unable to identify or verify the non-customer information, the IDI’s ATM is not required to display the official FDIC digital sign or the non-deposit sign after the non-customer uses their card and PIN (or similar credential) to access the ATM (i.e., status as a non-customer is determined).

(Updated August 16, 2024)

4. Is the FDIC official digital sign required at the top of all ATM screens?

Answer: In general, under 12 CFR § 328.4(c), an IDI’s ATM or like device that receives deposits for an IDI and offers access to non-deposit products must clearly, continuously, and conspicuously display the FDIC official digital sign as described in § 328.5 on its homepage or screen and on each transaction page or screen relating to deposits. As noted in 12 CFR § 328.5(f), an official digital sign “continuously displayed near the top of the relevant page or screen and in close proximity to the IDI's name would be considered clear and conspicuous.”

If the ATM does not offer access to non-deposit products, the final rule provides flexibility to meet the signage requirement, allowing the IDI to display the physical FDIC official sign by physically attaching it to the ATM instead of using the electronic sign on its homepage or screen. This is only an option for deposit taking ATMs or like devices, which do not offer access to non-deposit products, and that were put into service before January 1, 2025.

(Updated August 16, 2024)

5. If an ATM allows transfers of funds between deposit accounts but does not accept cash or check deposits, is the ATM subject to the sign requirements described in section 328.4?

Answer: No. The sign requirements in section 328.4 only apply to IDIs’ ATMs and other remote electronic facilities that “receive deposits,” and accepting cash or checks are examples of deposits.

(Updated December 2, 2024)

6. Where a non-bank owns and operates a bank-branded ATM (e.g., displays bank sign on top of the machine, bank’s name and logo is displayed on screen, etc.), is it permissible under part 328 for the ATM to display the FDIC official digital sign?

Answer: It depends. The FDIC has explained that display of the FDIC official digital sign by non-bank third parties is generally improper because display of the sign would imply that the non-bank is FDIC-insured. See 89 Fed. Reg. 3504, 3511-12 (Jan. 18, 2024). However, staff believes use of the FDIC official digital sign by a bank on non-bank owned, bank-branded ATMs does not raise this concern where the ATM includes a sufficient amount of a bank’s branding to clearly imply that the customer is doing business with the bank (e.g., there’s a bank sign on the ATM and the bank’s name and logo is on the ATM screen). In such cases, staff believes the FDIC official digital sign may be displayed on the ATM in a manner consistent with section 328.4.

(Updated December 2, 2024)

E. Social Media

1. Are IDIs required to post the new official digital sign on its social media advertisements?

Answer: No. IDIs are not required to display the FDIC official digital sign on its social media advertisements. IDIs should ensure that social media advertisements are compliant with the official advertising statement requirements contained in 12 CFR § 328.6.

(Updated July 15, 2024)

III. Technical Assistance

1. Where can IDI’s obtain additional information about the final rule to support compliance efforts?

Answer: The FDIC posted the slides from the FDIC’s banker webinar on Part 328 on its website.

The FDIC issued a Financial Institutions Letter and press release addressing the issuance of the final rule.

The final rule was published in the Federal Register on January 18th, 2024.

(Updated July 15, 2024)

2. Where can IDIs obtain downloadable versions of the digital official sign?

Answer: The FDIC has made optional versions of the official digital sign available for IDIs on FDICconnect, a secure website operated by the FDIC that FDIC-insured institutions can use to exchange information with the FDIC. The requirement to display the new FDIC official digital sign only applies to IDIs. Display of the FDIC official digital sign by any non-bank third party would improperly imply that the non-bank is FDIC-insured and would constitute a misrepresentation under part 328 subpart B.

(Updated July 15, 2024)

3. Where can an IDI obtain the FDIC’s consent to use non-English translations for the advertising statement?

Answer: The non-English equivalent of the FDIC’s official advertising statement (Member of FDIC, Member FDIC, FDIC-Insured) may be used in an advertisement only if the translation has received the prior written approval of the FDIC. 12 C.F.R. 328.6(f).

IDIs can send an email requesting prior written approval to translate the FDIC’s advertising statement to DepositInsuranceBank@FDIC.gov.

(Updated August 16, 2024)

IV. Compliance and Effective Dates

1. Are there any changes that had to have been implemented by the final rule’s April 1, 2024 effective date, or do IDIs have until January 1, 2025, to comply with all requirements?

Answer: On October 17, 2024, the FDIC announced that it is providing financial institutions additional time to get new process and systems in place by extending the compliance date for the new FDIC signage and advertising rule from January 1, 2025, to May 1, 2025. The extension applies only to a portion of the final rule designed to modernize the rules governing use of the official FDIC signs and advertising statements – Part 328, subpart A. However, IDIs can begin posting the official digital sign and implementing other aspects of the regulation prior to the compliance date for subpart A of part 328.

The compliance date related to the final rule’s amendments made to the prohibitions against misrepresentations of deposit insurance coverage, subpart B of part 328, remains January 1, 2025. Entities may implement the required subpart B changes prior to the January 1, 2025 compliance date. For example, some non-bank entities have updated their disclosures consistent with the amendments to part 328 subpart B.

(Updated December 2, 2024)

V. Advertising for Non-Deposit Products

1. In marketing materials that feature safe deposit boxes or credit products alongside insured products like checking accounts, should IDIs include a disclosure stating that these products are not FDIC-insured?

Answer: For the purposes of part 328, safe deposit boxes and credit products are excluded from the definition of “non-deposit product.” Therefore, there is no requirement under part 328 for an IDI to include such a disclosure in marketing material for these products.

(Updated July 15, 2024)