FDIC-Insured Institutions Reported Return on Assets of 1.11 Percent and Net Income of $66.8 Billion in the Fourth Quarter

- Full-Year ROA and Net Income Improved From 2023

- Quarterly ROA and Net Income Increased From the Prior Quarter, Driven By Higher Net Interest Income

- Community Bank Net Income Decreased Quarter Over Quarter

- The Net Interest Margin Rose Across All Asset-Size Groups in the Quarterly Banking Profile

- Asset Quality Metrics Remained Generally Favorable, Though Weakness in Certain Portfolios Persisted

- Loan Balances Increased Modestly From the Prior Quarter and a Year Ago

- Domestic Deposits Increased From the Prior Quarter, Primarily Due to Higher Uninsured Deposits

- The Deposit Insurance Fund Reserve Ratio Increased Three Basis Points to 1.28 Percent

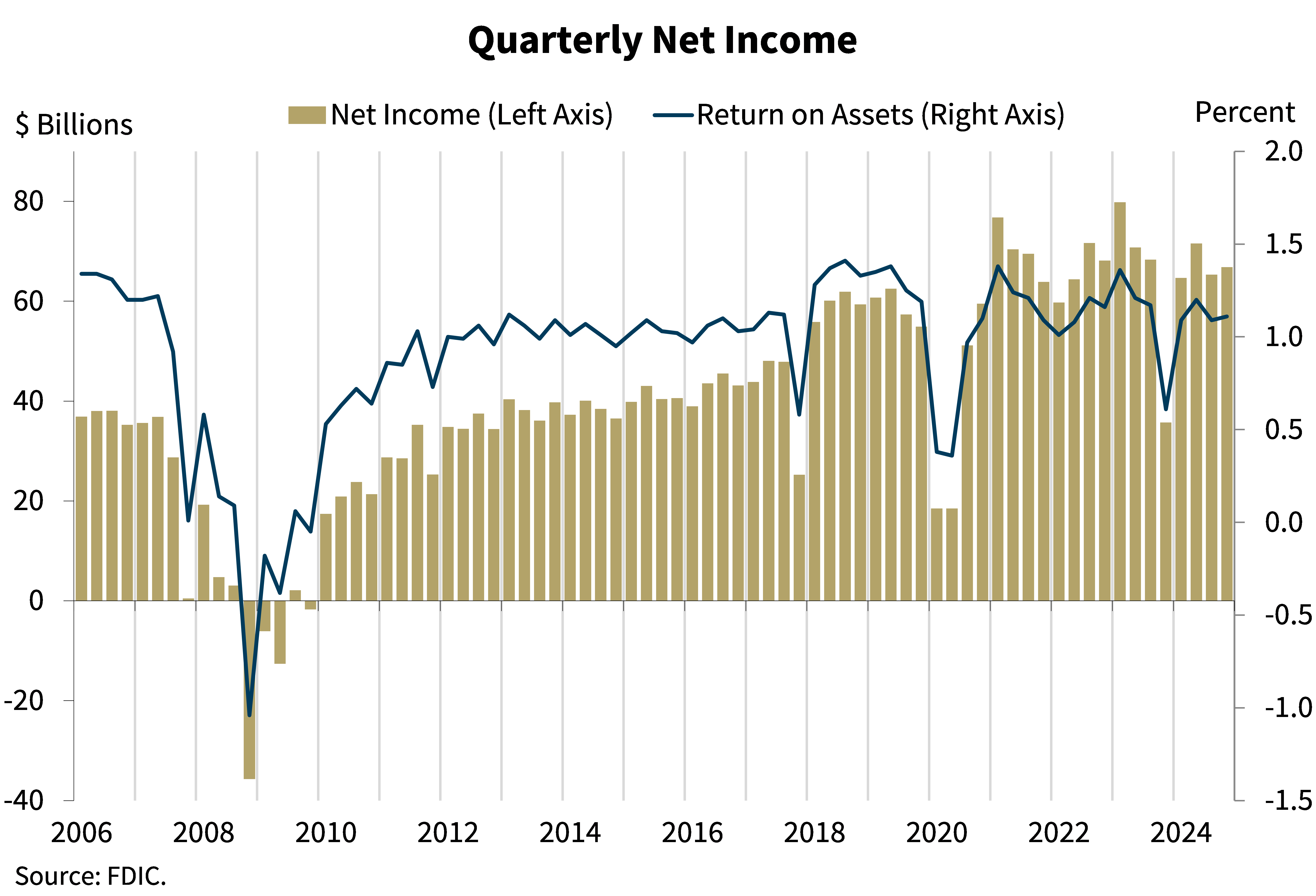

WASHINGTON— Reports from 4,487 commercial banks and savings institutions insured by the Federal Deposit Insurance Corporation (FDIC) reported a return on assets (ROA) ratio of 1.11 percent and aggregate net income of $66.8 billion in fourth quarter 2024, an increase of $1.5 billion (2.3 percent) from the prior quarter. An increase in net interest income drove the quarterly increase in net income. These and other financial results for fourth quarter 2024 are included in the FDIC’s latest Quarterly Banking Profile released today.

Highlights from the Fourth Quarter 2024 Quarterly Banking Profile

Full-Year ROA and Net Income Improved From 2023: The banking industry reported full-year 2024 net income of $268.2 billion, up $14.1 billion (5.6 percent) from the prior year, a level still well above the pre-pandemic average.1 The aggregate ROA ratio increased by three basis point to 1.12 percent. The increases in net income and ROA occurred primarily because one-time events in 2023 and 2024 led to lower noninterest expense, higher noninterest income, and lower realized securities losses in 2024.

Community banks reported full-year 2024 net income of $25.9 billion, down $624 million (2.4 percent) from the prior year. The decline was caused by higher noninterest expense, up $3.9 billion (6.1 percent), and higher provision expense, up $671 million (20 percent), which offset the increases in net interest income, up $2.2 billion (2.7 percent), and noninterest income, up $1.1 billion (5.9 percent). Community banks reported full-year pre-tax ROA of 1.14 percent, down eight basis points from the prior year.

Quarterly ROA and Net Income Increased From the Prior Quarter, Driven By Higher Net Interest Income: Fourth quarter net income for the 4,487 FDIC-insured commercial banks and savings institutions increased $1.5 billion (2.3 percent) from the prior quarter to $66.8 billion. The quarterly increase in net income was largely driven by an increase in net interest income, as declining short-term interest rates reduced interest expense more than interest income.

The banking industry reported an aggregate ROA of 1.11 percent in fourth quarter 2024, up 2 basis points from one quarter earlier and up 50 basis points from one year earlier.

Community Bank Net Income Decreased Quarter Over Quarter: Quarterly net income for the 4,046 community banks insured by the FDIC was $6.4 billion in the fourth quarter, a decrease of $441 million (6.5 percent) from third quarter 2024. Higher noninterest expense (up $931 million, or 5.4 percent) and realized securities losses of $565.9 million more than offset higher net interest income (up $774 million, or 3.6 percent) and higher noninterest income (up $187 million, or 3.7 percent). The community bank pretax ROA decreased 12 basis points from last quarter to 1.09 percent.

The Net Interest Margin Rose Across All Asset-Size Groups in the Quarterly Banking Profile: The industry reported a quarter-over-quarter increase in net interest income of $3.8 billion as the net interest margin (NIM) increased five basis points to 3.28 percent. All asset-size groups in the Quarterly Banking Profile reported a higher NIM in the fourth quarter. The industry’s fourth-quarter NIM was three basis points above the pre-pandemic average NIM. The community bank NIM of 3.44 percent increased nine basis points quarter over quarter, increasing for the third consecutive quarter, but is still below the pre-pandemic average of 3.63 percent.

Asset Quality Metrics Remained Generally Favorable, Though Weakness in Certain Portfolios Persisted: Past-due and nonaccrual (PDNA) loans, or loans that are 30 or more days past due or in nonaccrual status, increased six basis points from the prior quarter to 1.60 percent of total loans. The industry’s PDNA ratio is still below the pre-pandemic average of 1.94 percent. The PDNA ratio for non-owner occupied commercial real estate (CRE) loans declined five basis points to 2.02 percent, but the ratio remains 175 basis points above the pre-pandemic average. Despite declining slightly in the fourth quarter, the PDNA rate for non-owner occupied CRE loans remains elevated, largely driven by office loans at banks with more than $250 billion in assets. However, these banks tend to have lower concentrations of such loans in relation to total assets and capital than smaller institutions, mitigating the overall risk.

The industry’s net charge-off ratio increased three basis points to 0.70 percent from the prior quarter and is five basis points higher than the year-ago quarter. This ratio is 22 basis points above the pre-pandemic average. The credit card net charge-off ratio was 4.57 percent in the fourth quarter, up nine basis points quarter over quarter and 109 basis points above the pre-pandemic average.

Loan Balances Increased Modestly From the Prior Quarter and a Year Ago: Total loan and lease balances increased $105.0 billion (0.8 percent) from the previous quarter. The largest portfolio increases were reported in “all other” loans and loans to non-depository financial institutions, largely due to reclassifications following the finalization of changes to how certain loan products should be reported. Reclassifications also likely caused declines in other loan categories, particularly commercial and industrial (C&I) and consumer loans. In addition to these reclassifications, credit card loans and growth in loans to non-depository financial institutions contributed to the industry’s quarterly loan growth. The industry’s annual rate of loan growth remained steady in the fourth quarter at 2.2 percent.

Community bank loan growth was more robust and widespread than the industry. Total loans at community banks increased 1.3 percent from the prior quarter and 5.1 percent from the prior year, led by increases in nonfarm nonresidential CRE and residential mortgage portfolios.

Domestic Deposits Increased From Last Quarter, Primarily Due to Higher Uninsured Deposits: Domestic deposits increased $214.0 billion (1.2 percent) from third quarter 2024. Both savings and transaction deposits increased from the prior quarter, with declines in time deposits partially offsetting the increases. Brokered deposits decreased for the fourth straight quarter, down $46.0 billion (3.6 percent) from the prior quarter.

Estimated insured deposits increased slightly this quarter (up $39.1 billion, or 0.4 percent) while estimated uninsured domestic deposits increased $218.5 billion (3.0 percent). Growth in estimated uninsured deposits was widespread; most banks (60.1 percent) reported an increase in such deposits from the prior quarter.

The Deposit Insurance Fund Reserve Ratio Increased Three Basis Points to 1.28 Percent: In the fourth quarter, the Deposit Insurance Fund balance increased $4.0 billion to $137.1 billion. The reserve ratio increased three basis points during the quarter to 1.28 percent.

The Total Number of Insured Institutions Declined: The total number of FDIC-insured institutions declined by 30 during the quarter to 4,487. During the quarter, four banks opened, one bank failed, one bank failed after quarter end and did not file a Call Report, three banks did not file a Call Report after selling a majority of their assets to credit unions, one bank otherwise closed, and 28 institutions merged with other banks.

| 1 | The “pre-pandemic average” refers to the period of first quarter 2015 through fourth quarter 2019 and is used consistently throughout this press release. |