FDIC-Insured Institutions Reported Net Income of $59.7 Billion in First Quarter 2022

For Release

- Net Income Declined Year Over Year

- Net Interest Margin Remained Stable Quarter Over Quarter

- Loan Growth Was Broad-Based

- Credit Quality Continued to Improve

- Community Banks Reported a Slight Decline in Net Income Compared to the Industry

“The banking industry reported a decline in net income driven by an increase in provision expense. Capital and liquidity levels remain strong. In addition, loan growth and credit quality metrics remain generally favorable. Looking forward, inflationary pressures, rising interest rates and continued pandemic and geopolitical uncertainty will likely be headwinds for bank profitability, credit quality, and loan growth.”

— FDIC Acting Chairman Martin J. Gruenberg

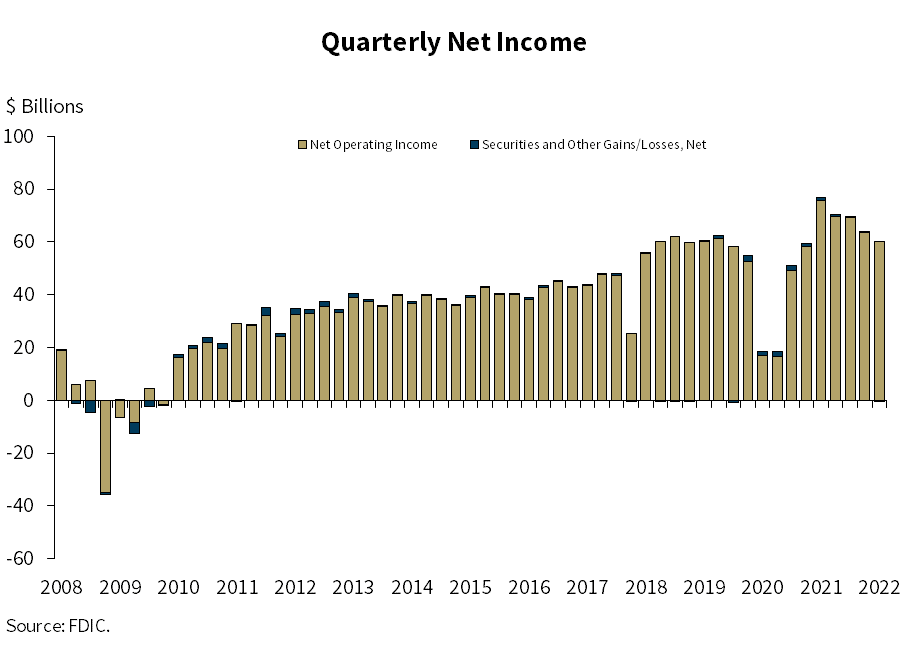

WASHINGTON— Reports from 4,796 commercial banks and savings institutions insured by the Federal Deposit Insurance Corporation (FDIC) reflect aggregate net income of $59.7 billion in first quarter 2022, a decline of $17.0 billion (22.2 percent) from a year ago. An increase in provision expense drove the annual reduction in net income. These and other financial results for first quarter 2022 are included in the FDIC’s latest Quarterly Banking Profile released today.

“In the first quarter, net income declined from the year-ago quarter as the banking industry raised provision expenses to reflect loan growth as well as economic and geopolitical uncertainty,” Gruenberg said.

Highlights from the First Quarter 2022 Quarterly Banking Profile

Net Income Declined Year Over Year: Quarterly net income totaled $59.7 billion, a decline of $17.0 billion (22.2 percent) from the same quarter a year ago, primarily due to an increase in provision expense. Provision expenses increased $19.7 billion from the year-ago quarter, from negative $14.5 billion during the same period a year ago to positive $5.2 billion this quarter. A majority of banks (62.8 percent) reported an annual decline in quarterly net income. The increase in provision expense also drove a decline of $4.1 billion (6.5 percent) in quarterly net income.

The banking industry reported an aggregate return on average assets (ROAA) ratio of 1.00 percent, down 38 basis points from the ROAA ratio reported in first quarter 2021 and down 9 basis points from the ROAA ratio reported in fourth quarter 2021.

Net Interest Margin Remained Relatively Stable Quarter Over Quarter: The net interest margin (NIM) declined by one basis point from the prior quarter to 2.54 percent. NIM was 4 basis points higher than the record low set in second quarter 2021 but 2 basis points lower than the level reported in the year-ago quarter. While more than half of banks (57.2 percent) reported higher net interest income compared with a year ago, NIM expansion was limited by earning asset growth, which continued to outpace net interest income growth.

The yield on earning assets declined to 2.70 percent (down 1 basis point from a quarter ago and down 7 basis points from a year ago) as the growth rate in average earning assets continued to outpace the growth rate in interest income. Average funding costs were unchanged over the quarter at the record low set in fourth quarter 2021 of 0.16 percent, but were down 4 basis points from the year-ago quarter.1

Community Banks Reported a Decline in Net Income: Community banks reported a decline in net income of $1.1 billion from the year-ago quarter, driven by a decline in revenue from loan sales. An increase in interest income on securities ($655.5 million, or 34.2 percent) and a decline in interest expense ($630.3 million, or 28.9 percent) drove an improvement in net interest income ($792.7 million, or 4.2 percent) from the year-ago quarter. However, net interest income declined slightly ($225.9 million, or 1.1 percent) from fourth quarter 2021. Provision expenses declined $129.7 million (31.0 percent) from a year ago and $64.4 million (18.3 percent) from the previous quarter. Most of the 4,353 FDIC-insured community banks (63.2 percent) reported lower quarterly net income compared with the year-ago quarter.

The net interest margin for community banks narrowed 15 basis points from the year-ago quarter to 3.11 percent, as growth in earning assets outpaced growth in net interest income.

Loan Balances Increased from the Previous Quarter and a Year Ago: Total loan and lease balances increased $109.9 billion (1.0 percent) from the previous quarter. The banking industry reported growth in several loan portfolios, including commercial and industrial (C&I) loans (up $81.3 billion, or 3.5 percent), nonfarm nonresidential commercial real estate (CRE) loans (up $28.2 billion, or 1.7 percent), and “all other consumer loans” (up $20.4 billion, or 2.0 percent).2

Annually, total loan and lease balances increased $531.8 billion (4.9 percent), as growth in consumer loans (up $192.6 billion, or 11.4 percent), nonfarm nonresidential CRE loans (up $98.0 billion, or 6.2 percent), and loans to nondepository institutions (up $91.3 billion, or 15.6 percent) offset a decline in C&I loans (down $62.5 billion, or 2.5 percent). Paycheck Protection Program loan forgiveness and repayment drove the annual decline in C&I loan balances.

Community banks reported a 1.3 percent increase in loan balances from the previous quarter, and a 2.1 percent increase from the prior year. Growth in construction and development and nonfarm nonresidential CRE loan balances drove the increases.

Credit Quality Continued to Improve: Loans that were 90 days or more past due or in nonaccrual status (i.e., noncurrent loans) continued to decline (down $4.5 billion, or 4.5 percent) from fourth quarter 2021. The noncurrent rate for total loans declined 5 basis points from the previous quarter to 0.84 percent. Total net charge-offs also continued to decline (down $3.0 billion, or 32.0 percent) from a year ago. The total net charge-off rate declined 12 basis points to 0.22 percent—just above the record low of 0.19 percent set in third quarter 2021.

The Reserve Ratio for the Deposit Insurance Fund Fell to 1.23 Percent: The Deposit Insurance Fund (DIF) balance was $123.0 billion as of March 31, down approximately $100 million from the end of the fourth quarter. The increase in unrealized losses on available-for-sale securities in the DIF portfolio, driven by the rising rate environment, was the primary reason for the decline. The reserve ratio fell to 1.23 percent due to both the decline in the DIF and growth in insured deposits.

Merger Activity Continued in the First Quarter: Forty-four institutions merged and no banks failed in first quarter 2022.

- 1

The record low average cost of funding earning assets cited in the fourth quarter issue of the Quarterly Banking Profile was 0.15 percent. Due to the effect of Call Report restatements subsequent to the publication, this ratio increased from 0.15 percent to 0.16 percent.

- 2

“All other consumer loans” includes single payment and installment loans other than automobile loans and all student loans.