FDIC-Insured Institutions Reported Reduced Profitability but Strong Loan Growth and Stable Asset Quality in First Quarter 2020

FOR IMMEDIATE RELEASE

- Loan and Lease Balances and Deposits Registered Strong Growth

- Asset Quality Metrics Remained Relatively Stable

- The Number of Banks on the "Problem Bank List" Remained Low

- Deteriorating Economic Activity Negatively Affected Banking Industry's Profitability

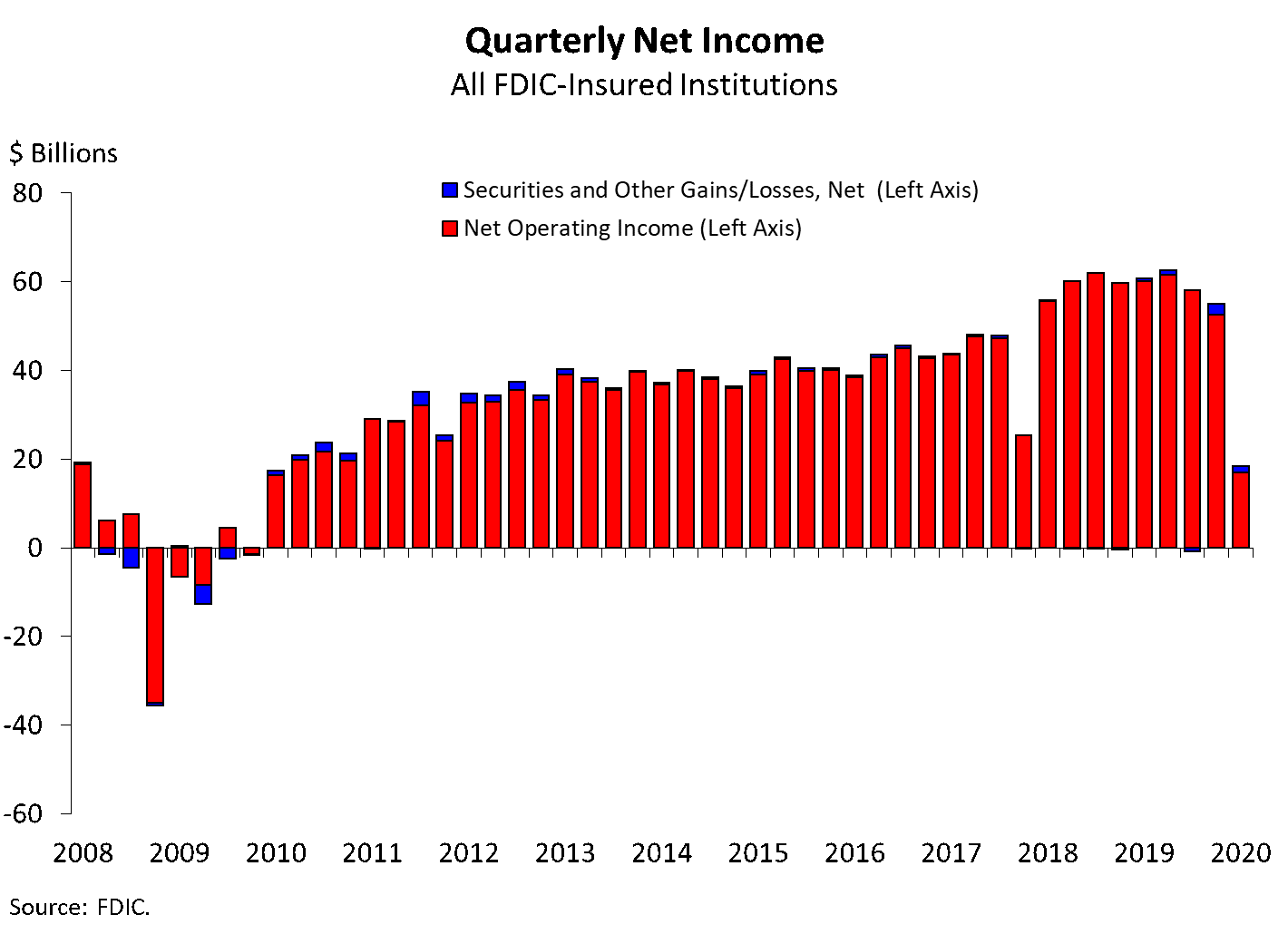

- Quarterly Net Income Fell by 69.6 Percent from First Quarter 2019

- Community Banks Reported a 20.9 Percent Decline in Net Income from a Year Ago

The banking industry has been a source of strength for the economy in the first quarter despite unexpected shocks. Although bank earnings were negatively affected by increases in loan loss provisions, banks effectively supported individuals and businesses during this downturn through lending and other critical financial services. — FDIC Chairman Jelena McWilliams

For the 5,116 commercial banks and savings institutions insured by the Federal Deposit Insurance Corporation (FDIC), aggregate net income totaled $18.5 billion in first quarter 2020, a decline of $42.2 billion (69.6 percent) from a year ago. The decline in net income is a reflection of deteriorating economic activity, which resulted in the increase in provision expenses and goodwill impairment charges. Financial results for first quarter 2020 are included in the FDIC's latest Quarterly Banking Profile released today.

"The banking industry has been a source of strength for the economy in the first quarter despite unexpected shocks. Although bank earnings were negatively affected by increases in loan loss provisions, banks effectively supported individuals and businesses during this downturn through lending and other critical financial services," McWilliams said.

"Notwithstanding these disruptions, at the end of the first quarter, bank capital and liquidity levels remain strong, asset quality metrics are stable, and the number of 'problem banks' remains near historic lows."

Highlights from the First Quarter 2020 Quarterly Banking Profile

Quarterly Net Income Fell by 69.6 Percent from First Quarter 2019: The 5,116 FDIC-insured institutions reported aggregate net income of $18.5 billion in first quarter 2020, a decline of $42.2 billion (69.6 percent) from a year ago. The decline in net income is a reflection of deteriorating economic activity, which propelled the increase in provision expenses and goodwill impairment charges. The decline was broad-based, as slightly more than half (55.9 percent) of all institutions reported year-over-year declines in net income. The share of unprofitable institutions increased from a year ago to 7.3 percent. The average return on assets ratio fell from 1.35 percent in first quarter 2019 to 0.38 percent in first quarter 2020.

Net Interest Margin Declined from a Year Ago to 3.13 Percent: The average net interest margin declined 29 basis points from a year ago to 3.13 percent. Net interest income declined by $2 billion (1.4 percent) from a year ago, with falling yields on earning assets contributing to the decline. Less than half (44.6 percent) of all banks reported year-over-year declines in net interest income.

Community Banks Reported a 20.9 Percent Decline in Net Income from a Year Ago: The 4,681 FDIC-insured community banks reported quarterly net income of $4.8 billion, representing a decline of $1.3 billion, or 20.9 percent. Provision expenses grew to $1.8 billion—three times the amount reported in first quarter 2019, hampering community bank profitability despite an increase in net operating revenue. Loan growth held steady at 5.8 percent year-over-year in spite of weakening economic conditions. The decline in average yield on earning assets surpassed the decline in average funding costs, causing the average community bank net interest margin to decline by 12 basis points to 3.55 percent.

Loan and Lease Balances Registered Strong Growth on Quarterly and Annual Basis: Total loan and lease balances increased by $442.9 billion (4.2 percent) from the previous quarter. Almost all major loan categories reported quarterly increases; however, the commercial and industrial loan portfolio reported the largest dollar increase, up $339.4 billion (15.4 percent). Over the past year, total loan and lease balances rose by 8 percent, the highest annual growth rate since first quarter 2008.

Asset Quality Metrics Remained Relatively Stable: Loans that were noncurrent (i.e., 90 days or more past due or in nonaccrual status) increased by $7 billion (7.3 percent) from the previous quarter. Commercial and industrial loans registered the largest dollar increase, rising by $3.6 billion (20.7 percent), but due to strong loan growth, the noncurrent rate increased only 4 basis points to 0.83 percent. The total noncurrent loan rate rose by 2 basis points from the previous quarter to 0.93 percent. Net charge-offs rose by $1.9 billion (14.9 percent) from a year ago, and the total net charge-off rate increased to 0.55 percent.

The Deposit Insurance Fund's Reserve Ratio Declined to 1.39 Percent: The Deposit Insurance Fund (DIF) balance totaled $113.2 billion in the first quarter, an increase of $2.9 billion from the previous quarter. The quarterly increase was led by unrealized gains on available-for-sale securities and assessment income. The reserve ratio declined 2 basis points from fourth quarter 2019 to 1.39 percent, due to the growth in estimated insured deposits.

The Number of Banks on the "Problem Bank List" Remained Near Historic Lows: The number of problem banks increased from 51 to 54 during the first quarter, the first quarterly increase since 2011. However, the number of problem banks remains near historic lows. Total assets of problem banks declined from $46.2 billion in the fourth quarter to $44.5 billion.

Mergers and New Bank Openings Continued in the First Quarter: During the first quarter, two new banks opened, 57 institutions were absorbed by mergers, and one bank failed.