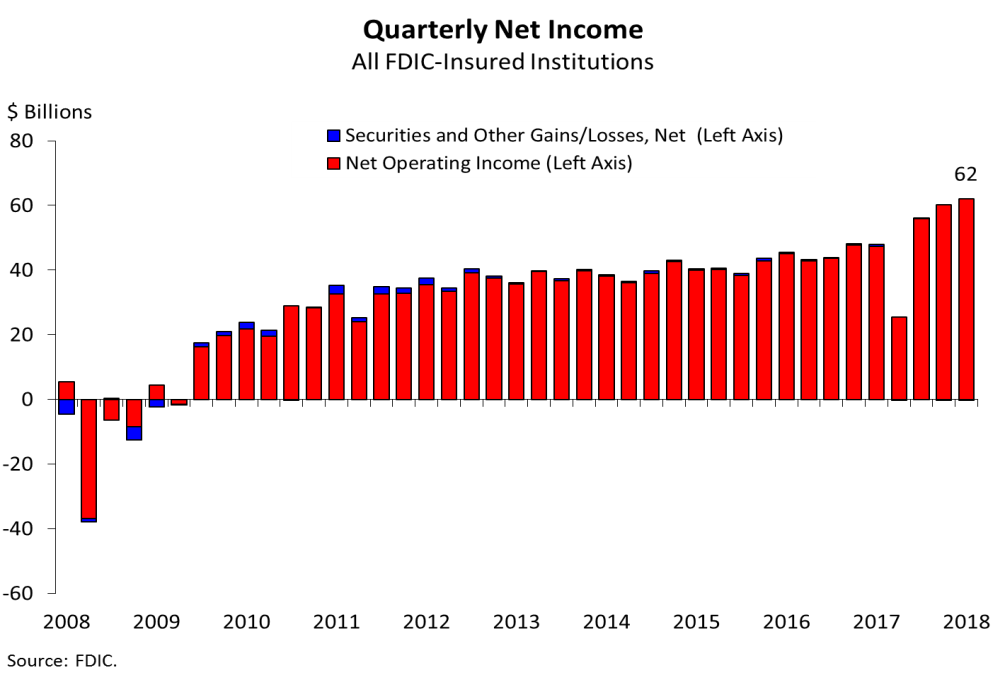

FDIC-Insured Institutions Reported $62 Billion in Net Income in Third Quarter 2018

FOR IMMEDIATE RELEASE

- Industry Net Income Registers a Strong Increase of 29.3 Percent from a Year Ago

- Higher Net Operating Revenue and a Lower Effective Tax Rate Boost Net Income

- Community Bank Net Income Rises 21.6 Percent from Third Quarter 2017

- Net Interest Margin Widens to 3.45 Percent as Asset Yield Increases Outpace Funding Cost Growth

- Annual Growth Rate for Loan and Lease Balances Is 4 Percent

- Noncurrent Rate Continues to Decline and Net Charge-Off Rate Remains Stable

"While the banking industry reported another positive quarter, we continue to monitor its overall performance in a rising interest-rate environment with competitive lending conditions."

-- FDIC Chairman Jelena McWilliams

Commercial banks and savings institutions insured by the Federal Deposit Insurance Corporation (FDIC) reported aggregate net income of $62 billion in the third quarter of 2018, up $14 billion (29.3 percent) from a year ago. The improvement in earnings was attributable to higher net operating revenue and a lower effective tax rate. Financial results for the third quarter of 2018 are included in the FDIC's latest Quarterly Banking Profile released today.

Of the 5,477 insured institutions reporting third quarter financial results, more than 70 percent reported year-over-year growth in quarterly earnings. The percent of unprofitable banks in the third quarter declined to 3.5 percent from 4 percent a year ago.

"The banking industry reported another strong quarter," FDIC Chairman Jelena McWilliams said. "Improvement in net income was led by higher net operating revenue and a lower effective tax rate. Loan balances grew, net interest margins improved, and the number of ‘problem banks’ continued to decline. Community banks also reported another positive quarter, with loan growth and a net interest margin surpassing the overall industry."

"While the performance results were strong, the extended period of low interest rates and the competition to attract loan customers have led to heightened exposure to interest-rate risk, and credit risk. Banks must maintain prudent management of these risks in order to sustain lending through the economic cycle."

Highlights from the Third Quarter 2018 Quarterly Banking Profile

Industry Net Income Registers a Strong Increase of 29.3 Percent from a Year Ago: Third quarter net income totaled $62 billion, an increase of $14 billion (29.3 percent) from 12 months ago. Improvement in net interest income and noninterest income, coupled with a lower effective tax rate, boosted the industry's net income. The average return on assets ratio rose by 29 basis points to 1.41 percent, the highest quarterly level reported by the industry since the Quarterly Banking Profile began in 1986.

Community Bank Net Income Rises 21.6 Percent from Third Quarter 2017: Reports from 5,044 insured community banks showed $6.8 billion in net income, reflecting an increase of $1.2 billion (21.6 percent) from a year earlier. This increase resulted primarily from higher net operating revenue and a lower effective tax rate. Higher net interest income (up $1.6 billion, or 8.9 percent) and higher noninterest income (up $110 million, or 2.4 percent) lifted net operating revenue by $1.7 billion (7.6 percent) from the third quarter of 2017. Community banks reported a decline in loan-loss provisions of $112.1 million (15.2 percent) and an increase in noninterest expenses of $855.1 million (6 percent).

Net Interest Margin Widens to 3.45 Percent as Asset Yield Increases Outpace Funding Cost Growth: Net interest income totaled $137.1 billion in the third quarter, an increase of $9.6 billion (7.5 percent) from a year ago. More than four out of five banks (83 percent) reported an improvement in net interest income from a year ago. The average net interest margin rose to 3.45 percent, up 15 basis points from a year ago, as average asset yields grew more rapidly than average funding costs.

Noninterest Income Grows Almost 4 Percent from a Year Earlier: Noninterest income rose by $2.4 billion (3.8 percent) from third quarter 2017, as more than half (54.2 percent) of all banks reported increases. The annual increase was led by servicing fees, investment banking fees, and other noninterest income.

Annual Growth of Loan and Lease Balances is 4 Percent: Loan and lease balances rose by $82.7 billion (0.8 percent) from the previous quarter, as all major loan categories registered growth. Over the past 12 months, loan and lease balances grew by 4 percent, a slight decline from 4.2 percent reported last quarter.

Noncurrent Rate Continues to Decline and Net Charge-Off Rate Remains Stable: The amount of loans that were noncurrent — 90 days or more past due or in nonaccrual status — totaled $101.3 billion, down $3.6 billion (3.4 percent) from the previous quarter. The largest declines in noncurrent balances were for residential mortgages (down $3.1 billion, or 6.3 percent) and commercial and industrial loans (down $1.1 billion, or 6.8 percent). The average noncurrent loan rate fell from 1.06 percent in the second quarter to 1.02 percent. Net charge-offs rose by $171.9 million (1.6 percent) from a year ago, led by an $837.8 million (12.3 percent) increase in net charge-offs for credit cards. The average net charge-off rate remained stable from a year ago (0.45 percent).

Number of Banks on the "Problem Bank List" Continues to Fall: The FDIC's "Problem Bank List" declined from 82 in the second quarter to 71, the lowest number of problem banks since third quarter of 2007. Total assets of problem banks fell from $54.4 billion in the second quarter to $53.3 billion. During the quarter, merger transactions absorbed 60 institutions, one new charter was added, and there were no failures.

Deposit Insurance Fund's Reserve Ratio Increases to 1.36 Percent: The Deposit Insurance Fund (DIF) balance rose by $2.6 billion during the third quarter to $100.2 billion, driven by assessment income. The DIF reserve ratio rose from 1.33 percent at the end of the last quarter to 1.36 percent. The third quarter of 2018 marks the last period that large banks will be assessed quarterly surcharges by the FDIC.

Congress created the Federal Deposit Insurance Corporation in 1933 to restore public confidence in the nation’s banking system. The FDIC insures deposits at the nation’s banks and savings associations, 5,479 as of September 30, 2018. It promotes the safety and soundness of these institutions by identifying, monitoring and addressing risks to which they are exposed. The FDIC receives no federal tax dollars—insured financial institutions fund its operations.

FDIC press releases and other information are available on the Internet at www.fdic.gov, by subscription electronically (go to www.fdic.gov/about/subscriptions/index.html) and may also be obtained through the FDIC’s Public Information Center (877-275-3342 or 703-562-2200).